Amid the COVID-19 pandemic, commentaries on finance have been peppered with the word “reset”, followed by an incredibly wide range of proposals as to what this “reset” may entail.

One common theme has been that financial technology will play a key role in the sector going forward. Mainland China strongly emphasises fintech in its financial development plan, and the central People’s Bank of China is running three-year fintech development plans. The 2019-2021 plan has just finished and the bank is now moving into the 2022-2025 plan.

The new plan seeks to further develop the mainland’s fintech sector and drive the economy’s digital transformation of finance over the next four years. The fintech development plan is based on the mainland’s 14th Five Year Plan, a roadmap for social and economic development between 2021 and 2025.

Global business services firm KPMG recently released its 2021 “China Leading Fintech 50 and Future 50” report, looking at the leading firms in the sector, giving an overview of the industry and discussing trends and prospects.

Cluster-based development

The KMPG study found that leading fintechs are heavily concentrated in three cities. Beijing (27%), Shanghai (25%) and Shenzhen (23%) remain at the top of the list, demonstrating a strong clustering effect. The big-three’s cumulative 75% fell seven percentage points from 2020 as other big cities such as Hangzhou and Chengdu become more attractive in the eyes of promising fintech enterprises.

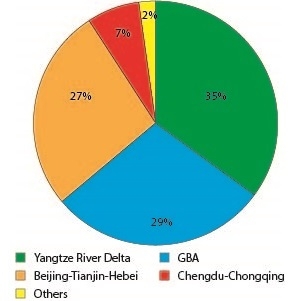

Geographically, the study revealed that almost all enterprises are in the top city clusters earmarked for priority development in the 14th Five-Year Plan – the Yangtze River Delta (35%), Guangdong-Hong Kong-Macao Greater Bay Area (29%), Beijing-Tianjin-Hebei (27%) and Chengdu-Chongqing (7%).

The ABCD technologies (artificial intelligence, blockchain, cloud computing and big data) remain core technologies for fintech enterprises. The percentage of companies that cited blockchain as a core technology rose to 49% in 2021, compared with 34% in 2020, as richer blockchain scenarios in finance attracted more attention to blockchain development during the year.

As the digital yuan pilot programme expands, user and transaction volumes have steadily increased, the study found. Following its official launch, the digital yuan will promote the development of the mainland’s digital economy, reshape the payment system, and help the central bank apply measures across various scenarios at the government, business and consumer levels.

KPMG also expected the digital yuan to boost innovation, provide important infrastructure for fintech companies and open up business opportunities for commercial banks and other financial institutions related to digital transformation. The digital yuan use may be extended to foreign exchange management and cross-border payments, as well being applied to the agriculture, education and urban construction sectors.

In the mainland, fintech’s steady progress has reduced the cost of financial services, and the development of big data, blockchain and other technologies has given rise to more secure and convenient payment methods like the digital yuan, while also lending solid technical support to development of the financial sector, KPMG said.

Top-50 selection

KPMG chose firms for its top 50 list based on innovation and transformation, popularisation of financial services, industry development prospects, capital market recognition, technology and data.

KPMG developed a start-up insights platform (SIP) model, which combines these core dimensions to evaluate enterprises from multiple dimensions including collaboration, technology, product, market and financing.

Platform technology empowerment (31% of selected companies) and wealthtech enterprises (17%) ranked first and second among selected firms in 2021, followed by inclusive technology and insurtech (both 13%). To highlight how fintech is returning to the basics of technological services, platform technology empowerment was divided into four sub-segments – integrated technology empowerment (6%); big data and AI (11%); blockchain, privacy computing and security (10%); and distributed computing, cloud computing and hardware acceleration (4%).

Economic driver

KPMG said finance is the lifeblood of the mainland economy, but the real economy is the ultimate driver of financial-sector development. Fintech, in the most basic sense, uses innovation to break two major pain points – information mismatch and high transaction costs – and promotes the development of the real economy, consumption and industrial upgrading.

In recent years, fintech development has boomed as new business models and scenarios have emerged. However, at the end of the day, fintech still aims to enhance market efficiency and rationally allocate resources.

Supply chain solutions

The global COVID-19 outbreak and regulatory changes presented significant challenges to global supply chains, and some domestic enterprises have even been forced to shut down for the time being. In this context, supply chain finance is playing a pivotal role in resolving the financing difficulties of micro, small and medium-sized enterprises and promoting stable supply chain development.

Historically, supply chain finance has been plagued by challenges, including large numbers of participants, interrelated participants and processes, and difficulties related to the identification of transaction scenarios. To address these issues, blockchain and electronic certificates can be used to connect supply chain participants and establish an alliance that includes upstream and downstream entities, finance companies, financial institutions, banks and other trade finance participants, the study report said.

Enterprises can use these technologies to digitalise assets such as accounts receivable, bills and warehouse receipts, and credit can then be granted to suppliers at different levels of the supply chain. In this way, blockchain can reduce financing costs and enhance capital efficiency across the entire supply chain.

Digital acceleration

Honson To, Chairman of KPMG China and Asia Pacific, said that based on the guidance provided by the development plan, during the past three years, the “four beams and eight columns” of fintech had been formed and the digital transformation of the financial sector had accelerated.

“2022 marks the sixth consecutive year in which KPMG has published the China Fintech 50. During this time, we have been pleased to witness the growth of so many outstanding fintech players. Going forward, we sincerely hope that the fintech industry will build an open, sustainable, scenario-based ecosystem under the guidance of national strategies that promote both prudent regulation and innovation.”

Jacky Zou, Vice Chairman and Senior Partner, Northern Region, KPMG China said new business models and scenarios had led to a fintech boom.

“The industry needs to focus on the essence of technological services and use technologies to break through the pain-points of traditional financial services,” he said. “The digital ABCD technologies were remaking great progress and have laid the foundation for the development of fintech infrastructure.”

Related link

Full KPMB report