The inflation currently sweeping across the globe is relatively muted in Hong Kong and Mainland China, but cost rises for raw materials energy are starting to have an impact on industries in the export-focused Guangdong-Hong Kong-Macao Greater Bay Area (GBA).

Respondents to the Standard Chartered GBA Business Confidence Index (GBAI) survey for the second quarter, conducted in association with the Hong Kong Trade Development Council (HKTDC), said inflation had joined COVID-19 in swaying their business prospects as global costs, especially for energy and commodities, move higher.

Input costs

Kelvin Lau, Senior Economist, Greater China, at Standard Chartered Bank , said raw materials were the top cost drivers for many businesses. Pressure also came from weakening external demand in April and May, the lingering effect of the Russia-Ukraine conflict, and from elevated global inflation eroding household spending power.

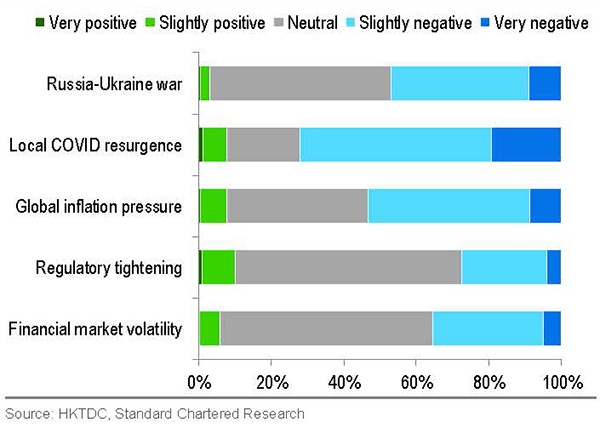

Asked about the impact of recent events, 72% of respondents saw slightly or very negative consequences from the COVID-19 pandemic. The second leading concern was inflation, with 53% concerned about global inflation pressure, and 47% about the impact of the Russia-Ukraine war. These were prominent challenges compared with financial market volatility (36%) and regulatory tightening (27%).

Of the five types of price pressure respondents faced, Mr Lau said 73% reported a rise in raw material costs over the year to date, closely followed by transport and logistics (72%) and energy (66%). GBA respondents also appear most impacted by higher raw material prices, with 54% reporting at least some degree of impact on their business, with transport and logistics (48%) and energy (43%) rounding up the top three spots.

Looking ahead, 61% of respondents expect raw material prices to rise further for the remainder of the year, followed by costs of transport and logistics (57%), energy (57%), wages (25%) and rent (24%). All this echoes the general market perception that broad-based inflationary pressure will continue as long as global monetary conditions stay loose and geopolitical and supply chain uncertainties linger – and this is likely to remain the biggest concern until superseded by fears over the risk of a global recession.

Cost profile

Asked to give a breakdown of their cost base, respondents said raw materials accounted for 29% of total costs on a mean basis, followed by wages (20%), and rent (15%). Rising transport and energy costs for the year to date have had a material impact on many GBA businesses, but the share of these costs in respondents’ overall cost bases is relatively low at 9% and 8%, respectively.

Unsurprisingly, cost structures vary across industries. Manufacturers, retailers and technology companies reported the highest shares of raw materials (39%, 31% and 29%, respectively), while services-oriented industries are more exposed to wage inflation (about 31% for both financial services and professional services). This is further reflected in the breakdown by city, with the more production-focused GBA cities in the mainland showing a higher proportion of raw materials in their cost base, while Hong Kong and Macao have a higher wage-cost component.

Mr Lau explained that GBA businesses have previously not been very successful in passing on higher costs to buyers, judging by weak profit performance and expectations, as well as thin surplus cash positions.

“We directly asked them about cost pass-through. Only 7.3% said they were able to pass on at least 50% of the cost increase to buyers, and another 37% said they were able to pass on less than 50%,” he said. “This leaves a material share of 41% reporting an inability to pass on higher costs, and only 15% saying they did not need to pass on costs. By industry, technology and retail respondents reported a higher share, with at least some pass-through rates of 62% and 52% respectively, versus only 24% for financial services.”

Tactical response

Asked how they dealt with rising inflation if they could not pass on higher costs to buyers, respondents listed several tactics. “Diversifying products/services” received the most votes (42%), followed by “cutting costs in other areas” (40%) and “streamlining/automation” (35%). More than 30% of votes went for “exploring suppliers/providers” and “upgrading products/ services”.

“We believe improving energy efficiency, relocating production and more hedging could gain more importance over time in fighting inflation,” Mr Lau said. “On a positive note, ‘reduction of scale’, of either headcount or inventory, was the least-chosen answer for now.”

Confidence weakened

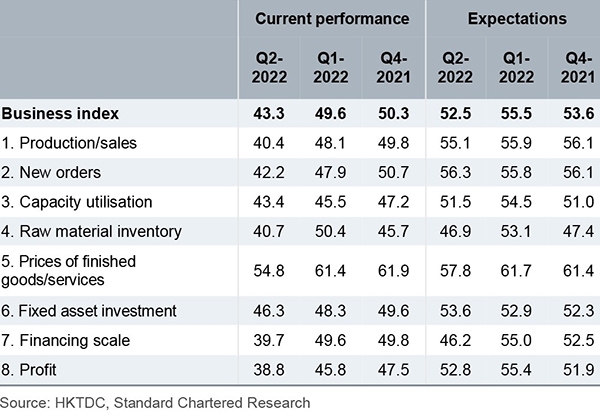

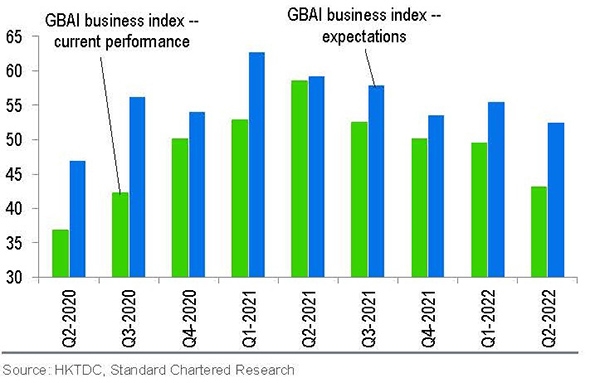

The overall GBAI, based on quarterly surveys of more than 1,000 companies operating in the GBA, showed that the current performance for “business confidence” weakened for a fourth consecutive quarter in the April to June quarter, falling further to 43.3 after marginally breaching the neutral 50 mark in the first quarter. This was also the lowest point since the third quarter of 2020 – not surprising given the latest survey was conducted in April and May, when the GBA’s businesses faced strong external and domestic headwinds.

In particular, April brought peak COVID disruption to production, sales and logistics across many GBA cities, even though they were spared from Shanghai-style lockdowns. Nonetheless, respondents still expect some form of a recovery in the coming quarter, although any recovery is likely to be moderate, at best, given the drop in the headline expectations index (to 52.5 from 55.5 prior, the weakest in two years).

A further breakdown of responses shows that not all sectors suffered equally from the still-present domestic and external headwinds. The “manufacturing and trading” and “retail and wholesale” sectors bore the brunt, while “innovation and technology” outperformed, possibly due to easing regulatory concerns. By city, all sub-indices endured the regional setback, including Hong Kong, which has seen its fifth COVID wave normalise since the start of the second quarter.

Credit indices reflected expectations of lower bank financing costs going forward, though overall credit conditions remain tight for now, especially due to the hit on cash flow positions.

Improving momentum

“We expect continued improvement in the growth momentum in June on Shanghai’s reopening and increased policy support more generally across regions,” Mr Lau said. “The government has stepped up efforts to revive the economy since late May, aiming to prevent GDP growth from slipping into negative territory in Q2 and to stem further increases in unemployment.”

Six of the eight main sub-components for business expectations fell quarter on quarter but only two dropped double digits to below 50 – raw material inventory (-12%) and financing scale (-16%).

Bringing the domestic COVID situation under control bodes well for the services sector, including retail and catering. The question is how much of a lift this might provide to the housing sector, given the persistent constraints of falling affordability, rising household debt and concerns over further housing price declines.

“We also expect infrastructure investment growth to accelerate to 10-15% in the coming months from about 7% year on year in May on normalising economic conditions and increased government support. President Xi Jinping recently called for infrastructure modernisation largely to drive growth this year following the COVID shock, but also in anticipation of slowing global growth as higher inflation and tighter monetary conditions start to bite,” Mr Lau said.

Related link

Full index